MBS Day Ahead: Are Bond Markets Reading From Same Scary Script?

There are no significant economic reports or scheduled events on tap for today. This will give us an opportunity to feel out the new trading ideas, not only for the rest of the week (which ends with Friday’s NFP), but for the month of October in general.

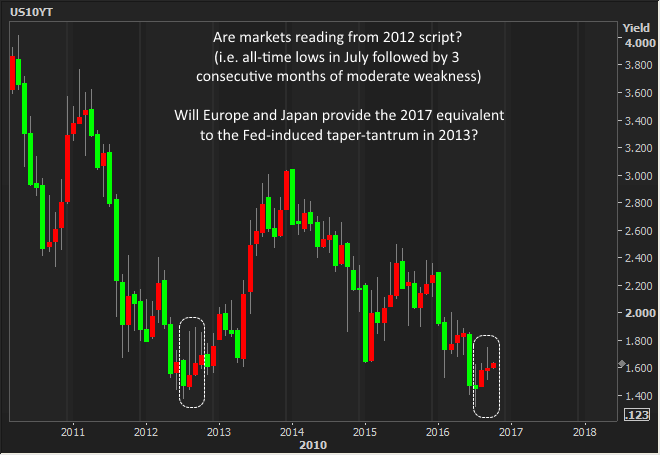

It turns out that October is historically an interesting month for markets. If you’ve been following rate movements closely for more than a few years, it likely has a negative connotation after having been etched into your memory as a bad month for 5 straight years beginning in 2008. True, things changed in 2013, but recall that it took a big “reset” in the form of the taper tantrum to pave the way for the past 3 years of gradual improvement.

The biggest question on every bond analyst’s mind is whether the past 3 years have been a “necessary correction” before the long-term trend toward lower rates continues, or whether we are setting ourselves up to repeat the 2012-2013 pattern of “all-time low in rates” followed by a few months of consolidation before a “shock” pushes rates significantly higher.

Eerily, rates hit all time lows in July of 2012 and 2016. Whereas we had the Fed and the taper tantrum providing the shock in early-mid-2013, this time around, we have the expiration of ECB bond buying in early 2017. After all, part of the recent move toward higher rates had to do with Draghi’s unwillingness to forcefully pre commit to more easing to follow the current scheduled round (how dare he!!).

In the following chart, each candlestick represents an entire month of trading in 10yr yields. Red means the month closed higher than it opened (i.e. a losing month).

Source: http://www.mortgagenewsdaily.com/mortgage_rates/blog/664982.aspx